Month: October 2024

Discovering Opportunities: A Week in Japan and the Promise of Yamagano

Junior Stock Review Weekly – October 9th, 2024

I’m ultra bullish on precious metals.

To me, gold and silver represent the best short-term opportunity to profit in the sector.

That is, if you pick the right companies.

I don’t think we’re at the point where the bullish tide floats all boats.

Maybe we will see that in the 2nd half of next year?

Even if the bullish tide in precious metals raises all boats, I strongly advise not buying mediocrity.

Stick to the best of the best companies.

It gives you the best chance of profiting consistently.

In reality, we’ve already seen the first push in the gold market – Q2 2024.

For myself and Premium subscribers, we saw a doubling of the value of the portfolio.

Winners like G Mining (GMIN:TSX) and Montage Gold (MAU:TSXV) returned close to 200%.

These are HUGE wins to have early on in a bear market reversal.

Early moves in a bull market are all based on sentiment.

Typically, the metal price moves first.

Optimism about the future grows and money is deployed into the equities.

The best companies are the first to rise.

The early investors make the money and the FOMO of investors on the sidelines grows.

This is how a bull market begins.

While the move in Q2 was good, I don’t think it’s the big sentiment change that we’re waiting for.

That main reversal is still to come.

Being contrarian matters in the junior resource sector.

As Rick Rule puts it, “you’re either contrarian or you will be a victim”.

Wise words.

But being contrarian isn’t easy.

You have to be patient and, in many cases, courageous.

Buying companies in a sector that is hated is tough.

The gold markets of the last 10 years are a perfect example.

We had gold bull runs in 2016 and 2020.

Each one was only about 8 months in duration.

It was quick and a ton of money was made in a short time frame.

Heck, 2020 was the best financial year of my life.

But look at the duration of time in between bull runs, around 4 years between both.

For the investors who bought right and were patient, it was life changing.

I’m the perfect example;

In 2013, I sold my house and used 2/3rds of the equity to buy junior mining companies.

I had to wait 3 years, but in 2016, I was paid back – big time!

I left my career in steel manufacturing to pursue investing full-time and have never looked back.

Pick right and sit tight as they say.

So what’s the next metal to go on a bull run?

It’s a great question.

A question that all resource sector investors need to be asking themselves.

In my view, there are a couple of metals that are hated and ripe for a reversal down the road.

The first is the platinum group of metals (PGMs).

Rightly, PGMs are most associated with their use within catalytic converters.

Catalytic converters are used in internal combustion engine (ICE) vehicles.

They’re used to capture harmful metals from the exhaust of the fossil-fuel burning engines.

Essentially, they scrub the exhaust fumes, making them cleaner.

Very useful and necessary.

The problem is, there’s nothing more hated or negatively forecasted than ICE vehicle sales.

Hence, the demise of the PGM prices and equities.

The PGM prices have fallen off a cliff.

Especially palladium.

It has been a violent crash from its highs.

Source: TradingEconomics.com

While the PGM prices are down significantly, it’s nothing compared to the carnage in the equities.

In many cases, you have companies with resources that are selling for pennies on the dollar.

Single digit MCAPs.

It’s incredible.

These are the opportunities you find in a sector that is hated or forgotten.

Now, I’m not going to say that the PGM prices can’t stay depressed for months or years to come.

They can.

There is a bearish case for PGMs that will be hard to break.

The big barrier to break is investors’ outlook for electrification.

Mainly, the future adoption of EVs.

Your first thought might be, “that is going to be impossible”.

I disagree, to a point.

I don’t think the world is going to stop electrifying.

That’s something that should and will happen over time.

I just think that it’s going to take MUCH longer than expected.

Ideas of net carbon zero by 2050 are crazy.

It’s impossible.

There are 2 massive hurdles;

First, the cost.

Second, the time it takes to construct the infrastructure.

It will take trillions and multiple decades to accomplish.

It will be done, but we’re looking at 2100, not 2050.

I think investors will start to see the reality of electrification.

More importantly, I think they will see the importance of ICE vehicles to bridge the gap.

Especially in emerging markets.

Second and 3rd-world countries will become wealthier over time.

With that wealth will come the want and need for a vehicle.

ICE vehicles are the cheapest and easiest form of transportation to acquire and use.

ICE vehicle sales will fall over time, but it’s going to be multiple decades in the future.

Next, and this is a very short-term concern, a recession would impact the economy and hence demand for goods and services.

Any base or industrial metal would have its demand affected by a downturn.

That said, the government’s playbook for dealing with recessions is straightforward;

Lower interest rates and infuse money into the economy.

Rinse and repeat until the economic outlook turns.

If there’s a recession ahead, this is how they will deal with it.

2009 and 2021 are prime examples.

Both years followed a crash in the market and recession fears.

Both years ended up causing booms in metal prices.

If a recession or a crash is ahead, I expect the playbook to be exactly the same.

While the bearish case is still firmly in place, there are reasons to be optimistic.

One of the biggest reasons comes from PGM supply.

The bulk of the world’s PGM supply is produced in Russia and South Africa.

I don’t think it’s a stretch to think that the Russian supply could be in jeopardy in the future.

Tensions with Ukraine and the rest of the West seem to only be increasing.

Interruption to the Russian PGM production would be beneficial to the PGM price.

Finally, it all comes down to price.

The cure for low prices is low prices.

Low metal prices cause production to be reduced.

Lower production means that demand has to be met with inventory.

Falling inventory and mine supply can only go on for so long.

After enough time, the price must go up to encourage production.

In my view, this is where we are with the PGMs.

So how do you profit from the potential turn in the PGM market?

Good question.

You can buy the physical metal or invest in a trust or ETF.

Kitco and Sprott Money sell PGM coins and bars.

In terms of a trust or ETF, there’s the Sprott Physical Platinum and Palladium Trust (SPPP-U).

Or you can speculate in the junior PGM equities.

There aren’t a lot of them out there.

The key is to pick the right one(s).

Junior Stock Review Premium subscribers are always the first to hear my investment ideas.

In fact, I came up with the contrarian PGM idea a couple months back.

In the months since, I have narrowed my focus down to a couple companies.

Those companies are on the Premium Watchlist and may become a new pick soon.

If you’re interested in learning about the PGM companies I’m looking at, consider subscribing to Junior Stock Review Premium.

For a limited time, I’m offering 20% OFF Premium by using the coupon code: SAVE20 on both the quarterly and yearly subscriptions.

The Gignac Family

People, people, people.

It’s often cited yet not always adhered to by investors.

The business plan for a junior resource company must match the management team’s core competencies.

If you are exploring for minerals, you better have a strong geological acumen.

Conversely, if you are looking to build a mine, you better have the knowledge, skill and experience.

Mine building isn’t easy, there is plenty that can go wrong.

In both instances, finding the best people at exploration or mine development isn’t easy.

It isn’t easy because there just aren’t a lot of them out there.

Therefore, when you do find the right people, stick with them.

Over my investing career, this has been arguably my biggest strength.

Invest in the people that I know are trustworthy, competent and that I have made money with.

Today, I will introduce the Gignac family.

In my view, it all starts with Louis Gignac Senior.

Gignac Senior was the founder of Cambior Inc., back in 1986.

Over the next 18 years, Cambior grew into a mid-tier gold producer.

It reached almost 700Koz of gold production in 2004.

Eventually, Cambior merged with IAMGOLD and a new path was laid out for the Gignac family.

Gignac Senior started G Mining Services with his 3 sons, Louis-Pierre, Mathieu and Michael.

Since 2006, G Mining Services has been sought out for their technical mining services.

Their track record speaks for itself, as they have numerous examples of success around the world.

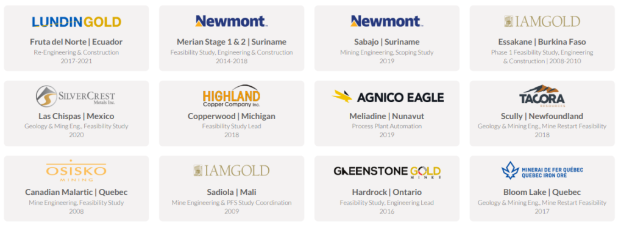

Take a look below and I’m sure you will recognize some of the mines they have built.

G Mining Services’ latest success story is the construction of the Tocantinzinho gold project in Brazil.

This time, the successful build means so much more, as it was for a new emerging mid-tier producer – G Mining Ventures (GMIN:TSXV).

G Mining Ventures is led by Louis-Pierre (LP), who is looking to follow in his dad’s footsteps.

LP’s vision to grow G Mining took a big step forward in July with the acquisition of Reunion Gold.

Reunion’s Oko West project is big and has the capacity to move G Mining into the multi-asset mid-tier producer realm.

Reunion’s acquisition was not only big for G Mining, but also brought some big attention to Guyana.

There is more M&A to come in the region.

To hear more about that and coverage on G Mining, subscribe to Junior Stock Review Premium.

For a limited time, I’m offering 20% OFF Premium by using the coupon code: SAVE20 on both the quarterly and yearly subscriptions.

Next Week’s Newsletter

Being contrarian is the key to being a successful resource sector investor.

This week, I gave my view on the PGMs.

Next week, I will give you a breakdown on another metal that I think is a good contrarian bet.

In addition to that, I will introduce you to another person who is making big waves in the resource sector.

It’s all about the people.

Stay tuned!

If you’re not already, consider becoming a FREE subscriber to Junior Stock Review Weekly by going back to the home page and scroll down the page until you reach “Free JSR Newsletter”.

Enter you email address and confirm it in Mail Chimp – you’ll never miss an issue!

MUST-see Media

- MSE Interview with Fund Manager Willem Middelkoop of the Commodity Discovery Fund

- Field Notes Episode #2 – FPX Nickel Corp. and the Future of Mining in British Columbia

![]()

Interested in becoming a Premium subscriber?

Use the coupon code: SAVE20 to receive 20% off a quarterly or yearly subscription.

Here are the answers to a few of the most commonly asked questions about the newsletter;

- Choose from a Quarterly or Yearly Subscription Option

- Choose what’s right for you, whether you want to test drive for 3 months or maximize your benefit with a yearly subscription.

- Weekly Market Updates are sent directly to your inbox with junior resource sector commentary and news on the companies in the Premium Portfolio.

- Get access to all prior issues of Premium and take full advantage of years of market research and commentary.

- Portfolio company rankings with buy at or below pricing, plus % allocations of each position.

- Q&A – I answer all of my subscribers’ questions!

- The Diligent Speculator Video Series – A Bonus for Yearly subscribers only, learn about geology & deposit types, exploration techniques, mineral processing and metallurgy, balance sheets and much more.

Subscribe to Junior Stock Review Premium

Still have questions? You can email me personally here: juniorstockreview@gmail.com

Market Update – October 9th, 2024

Junior Stock Review Weekly – October 7th, 2024

Perfecting your craft as an investor, especially in the junior resource sector, is a continual process.

For me, it’s something I’ve been working on full-time for the last 8 years.

One lesson that needs to be learned as quickly as possible is how important the people are to the success of a junior company.

Without good stewardship, a junior company is rudderless and doomed for failure.

Sometimes, the good people are overshadowed by the geology – exceptional drill results.

Investors forget that it was the management that picked the project and planned the exploration program.

Good people know what they’re looking for.

And, once they’ve found it, they systematically work at revealing its value.

But, the story isn’t done there, communication with the market is paramount – turns out the best people are good at that, too.

Currently, the resource market is littered with high quality management teams, with top-tier projects and are selling at a discount to the metal price.

This situation isn’t new to me.

I’ve been here before.

I had the patience and the know how to pick the good companies and, ultimately, changed the course of my life.

A Bull Market in 2024?

For me, the stretch of time between 2013 to 2016 is unforgettable.

It was the deepest bear market I had ever encountered.

I had sold my house and used ⅔ of the equity to buy a select group of junior mining companies.

Over those 3 years, I saw my portfolio fall by more than 30%.

It was tough, I often wondered if I did the right thing.

Turns out, I did – 2016 was incredible.

The funny thing is, I didn’t even see it coming.

Rick Rule has often told me, and I’m paraphrasing, “investors’ outlook is influenced by the immediate past.”

It’s so very true.

For 3 years, all I knew was a falling market.

Companies would release good news and the share prices would fall – it was a liquidity event.

Worried investors were using the good news to capture volume and sell down their positions.

Sound familiar?

It should.

2022 and 2023 were eerily similar to 2014 and 2015.

Much like that period of time, I think today feels a lot like early 2016.

For those who don’t remember or weren’t in the market at that time, 2016 was the start of a bull market that changed my life.

I had hand picked a select portfolio of what I thought were the best of the best junior mining companies.

That portfolio returned roughly 300% over that next year.

With that windfall of profits, I left my career in steel manufacturing to pursue investing full time.

It’s now been 8 years since I made the leap toward my own personal freedom and I could never go back.

When I look at the market today, my experience tells me we’re in for another one of those life-changing years in 2024.

Precious metals prices continue to trend upward while the junior mining companies are lagging behind.

This is where the opportunity is.

Just like in 2014 and 2015…if you can pick the right companies.

Speaking of picking the right companies, I will share with you the biggest win of my investing career so far.

It’s AbraSilver (ABRA:TSXV).

I first identified AbraSilver back in 2019.

It was selling for C$0.025/share.

The market hated it, completely disinterested.

But I saw something more.

I saw a company with a brand new management team – CEO John Miniotis and VP Exploration David O’Connor.

These men’s pasts were decorated with success and having met John in person, I knew he was the right man to lead ABRA and develop Diablillos into a future mine.

The people part of the equation was filled.

Next, I could see that they had a small but expandable gold and silver oxide resource.

Exploration potential captures market attention almost regardless of the overall market sentiment.

Having it is a huge plus for any junior mining company.

The project, Diablillos, is located in Salta, Argentina.

Rightfully, there are question marks surrounding Argentina and its mining investment attractiveness.

I don’t disagree.

But, when a company has the right people and project, and is selling for less than its worth, to me, it’s an opportunity.

Finally, I was able to recognize where precious metals prices were headed and how AbraSilver’s story would attract market attention.

I then bought shares in the open market and participated in their next 2 financings, which occurred in the heart of the Covid panic.

In just over a year, AbraSilver’s share price hit a high of C$0.82/share and returned the biggest win of my career so far – $0.025 to $0.82 = 32x!

Today, I still own and cover AbraSilver in Junior Stock Review Premium.

They now have 209Moz silver equivalent ounces in their Reserves and I think have the potential to add a lot more.

Not only this, but a major mining company, Kinross (K:TSX), just recently took a 9.9% stake in the company.

Without a doubt, AbraSilver is a top-tier acquisition target by all the senior precious metals mining companies.

Will 2025 be the year they get taken out?

I certainly wouldn’t be surprised if it were.

Precious metals prices look like they should remain strong and I think that bodes well for M&A.

Senior producers are continually depleting their reserves and, therefore, have to replace them.

In my view, AbraSilver will be at the top of the list when it comes to M&A targets.

To follow AbraSilver’s news flow and get my view on where things are headed on a weekly basis, subscribe to Junior Stock Review Premium.

For a limited time, I’m offering 20% OFF Premium by using the coupon code: SAVE20 on both the quarterly and yearly subscriptions.

Field Notes YouTube Video Series

Last August, I started a YouTube video series titled, Field Notes.

The series is all about my journey as an investor in the junior resource sector.

More specifically, I take you along into the field to the companies’ projects that I’m personally invested in.

Site visits aren’t something that every investor gets to do, yet they are incredibly useful and important in the process of picking good investments.

Seeing the lay of the land, meeting the locals surrounding the project and getting to spend extended 1 on 1 time with management can’t be beat.

Field Notes fills that gap for the investors who can’t make it to the site.

In Episode #1, I share my story and how I used the junior resource sector to gain the personal freedom that I enjoy today with my family.

Check it out and, if you like, please subscribe and support the channel.

MUST-see Media

- Rick Rule’s Keynote Speech from Precious Summit in Beaver Creek, Colorado

- Strategic Speculations: The Next 12 Months (MIF Vancouver, Sept.21st)

![]()

Interested in becoming a Premium subscriber?

For a limited time, I’m offering 20% OFF Premium by using the coupon code: SAVE20 on both the quarterly and yearly subscriptions.

Here are a few of the answers to the most commonly asked questions about the newsletter;

- Choose from a Quarterly or Yearly Subscription Option

-

- Choose what’s right for you, whether you want to test drive for 3 months or maximize your benefit with a yearly subscription.

-

- Weekly Market Updates are sent directly to your inbox with junior resource sector commentary and news on the companies in the Premium Portfolio.

- Get access to all prior issues of Premium and take full advantage of years of market research and commentary.

- Portfolio company rankings with buy at or below pricing, plus % allocations of each position.

- Q&A – I answer all of my subscribers’ questions!

- The Diligent Speculator Video Series – A Bonus for Yearly subscribers only, learn about geology & deposit types, exploration techniques, mineral processing and metallurgy, balance sheets and much more.

Subscribe to Junior Stock Review Premium

Still have questions? You can email me personally here: juniorstockreview@gmail.com