Solitario Exploration & Royalty: Offering A Great Value Proposition in this Zinc Bull Market

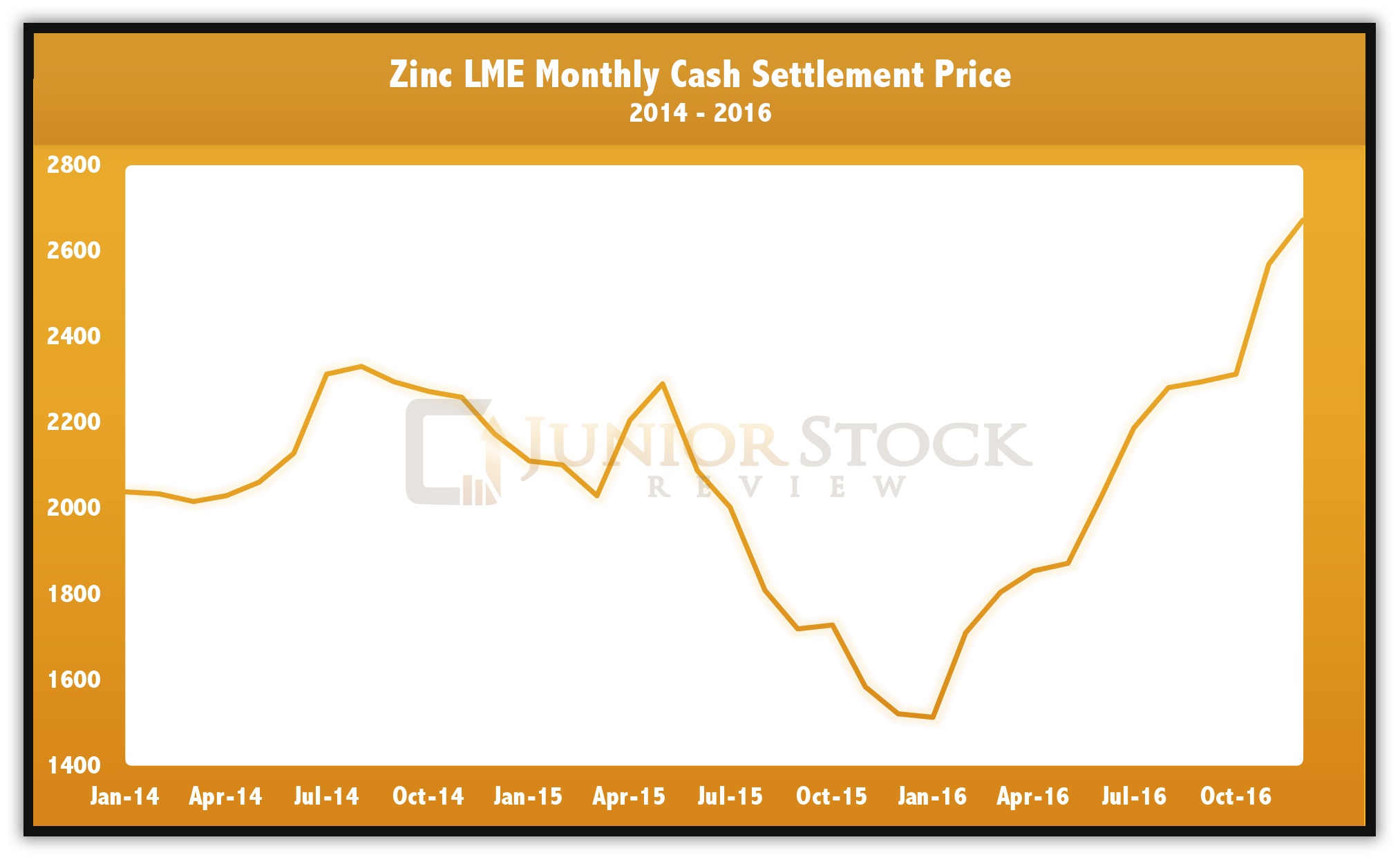

I’m bullish on the price of zinc. For those who may have missed it, here’s a link to Part 1 and Part 2 of Zinc’s Bullish Narrative, which I wrote last month. After hitting a low of $0.66/lbs in the beginning of 2016, the zinc price rose off of its bottom, hitting a high of $1.33/lbs early in 2017.

Source: London Metals Exchange

The price has since corrected, currently sitting at roughly $1.12/lbs, and a lot of people are asking, ‘is the zinc bull market over?’ In my opinion, definitely not.

Simply put, inventories are still falling without the aid of new supply coming online. I believe the cure for low prices is low prices, and while that still may be a few months away, I’ve found a company which has interests in a highly leveraged zinc deposit in a great mining jurisdiction. It gets even better, because their 30% interest in the project is further strengthened by the fact that they will not have to pay a cent in the development of the asset, right through to production as Milpo will lend Solitario the construction funding necessary to maintain its 30% interest in the project.

Further, this company is currently awaiting the conclusion of a deal with another large, high-grade zinc deposit, which sits at the foot of the giant zinc mine, Teck’s Red Dog.

This company is cashed up and led by an experienced and savvy management team, which is dedicated to bringing value to its shareholders. This company is Solitario Exploration and Royalty Corporation.

Let’s take a closer look!

Solitario Exploration and Royalty (SLR:TSX, XPL:NYSE)

MCAP – 38.6 million (at the time of writing this report)

Shares – 38,685,189

Fully Diluted – 38,685,189

Cash – roughly USD $17 million in cash or cash equivalents – Q1 Financial Report shows $14.9 million in short-term investments, which I’m told are U.S. Treasury Securities and Bank CDs.

Solitario’s People

Solitario is led by CEO, Christopher E. Herald, who is a geologist by trade, having received a B.Sc. in geology from the University of Notre Dame, and a M.Sc. in geology from the Colorado School of Mines. Herald has been with Solitario since 1992, starting out as a Director and then taking on the CEO position in 1999. Prior to Solitario, Herald was President and CEO of Crown Resources Corp., which was sold to Kinross Gold. Prior to Crown, Mr. Herald was a senior geologist with both Echo Bay Mines and Anaconda Minerals.

Walter H. Hunt is Solitario’s COO, a position he has held since 2008. Hunt’s work history is closely tied to Herald’s, having worked for Echo Bay Mines, Anaconda and Noranda in various senior roles. Hunt is a geologist by trade, having received his B.Sc. from Furman University, and a M.Sc. from the Colorado School of Mines. Before becoming COO of Solitario, Hunt was VP of Operations and President of Solitario’s South American Operations, positions he held since 1999.

Solitario’s Corporate Officers are rounded out by James R. Maronick, who is the company’s CFO. Maronick is an accountant by trade, having received a B.A. in accounting from the University of Notre Dame, and a M.A. in finance from the University of Denver.

NOTE: Solitario is formerly the South American portion or subsidiary of Crown Resources, of which Herald, Hunt and Maronick were all a part. Crown owned the Buckhorn Mountain Gold Project in Washington State, which was sold to Kinross in 2006 for around $220 million. Solitario is now the sole focus of the management team, a team which has led the company through multiple commodities cycles, while minimally diluting its shareholders; not many companies are able to check off those two boxes!

Solitario’s management has set itself up well to capitalize on a zinc market which, in my opinion, is set to get hot as supply is falling short of demand. Let’s take a look at the properties in which Solitario has an interest.

Properties

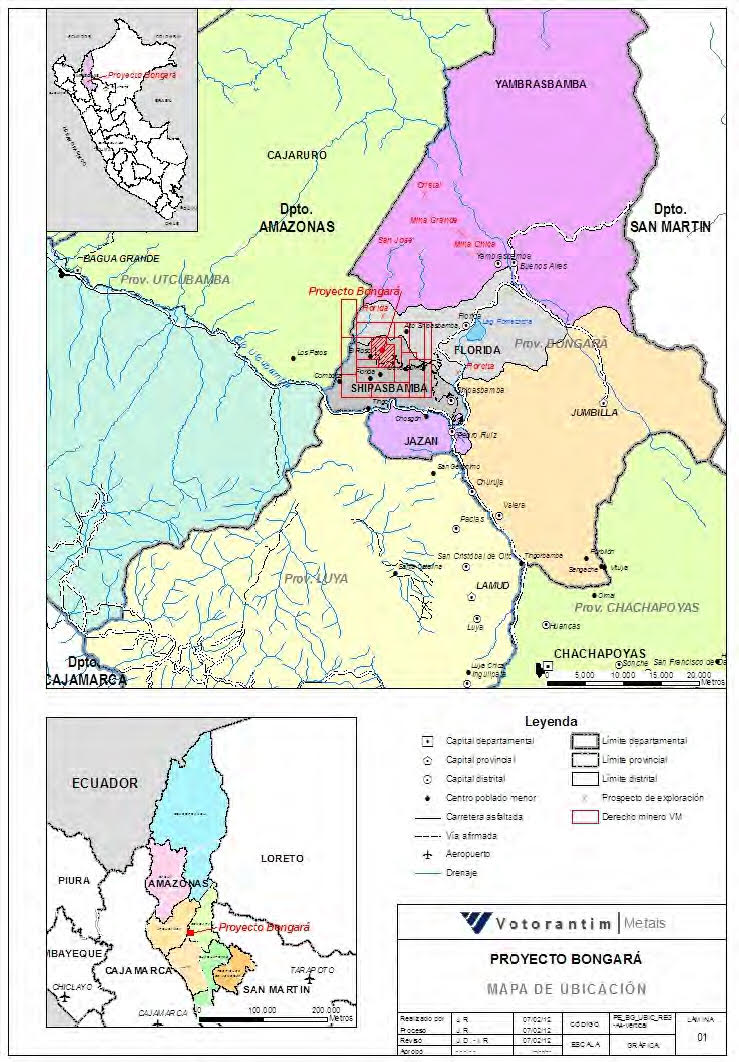

Bongará Zinc Project

- The Bongará Zinc Project is located in the Eastern Cordillera of Peru at the sub-Andean front in the upper Amazon River Basin. 680 km north-northeast of Peru’s capital Lima and 245 km northeast of Chiclayo.

Source: 43-101 Technical Report – pg.4

- The location of Bongará is remote, which will certainly add cost to the infrastructure needed to run a mine. Workforce for a mine is another potential question mark. The Technical Report says the following,

“High-relief terrain and high annual rainfall are conditions affecting development, especially in the area of infrastructure construction and process/tailings containment and stability. Politically and socially, however, the development of a mining operation at this location is considered low risk as many of the local residents are already employed or seeking employment with Votorantim.” ~43-101 Technical Report – pg. 137

- By the end of 2017, the project will be fully accessible from the main highway via a 35 km road. In addition, further road construction will be completed on the property, as Milpo will construct roads to access some of the deeper areas of the property for exploration.

- In the Technical Report, the remoteness of the project brought into question the power source for the future mine. In the report, they refer to the construction of the Bagua/Jaen power station as a possible power source. Via email, I corresponded with Soliatrio’s Investor Relations Director, Debbie Mino-Austin. In our correspondence, she said that access to power shouldn’t be an issue and that the Bagua/Jaen power station had been completed. It’s likely, however, that a mini-hydroelectric plant on the Utcombamba River will be constructed for Bongará power (mini hydroelectric plants are common in Peru and relatively inexpensive to construct).

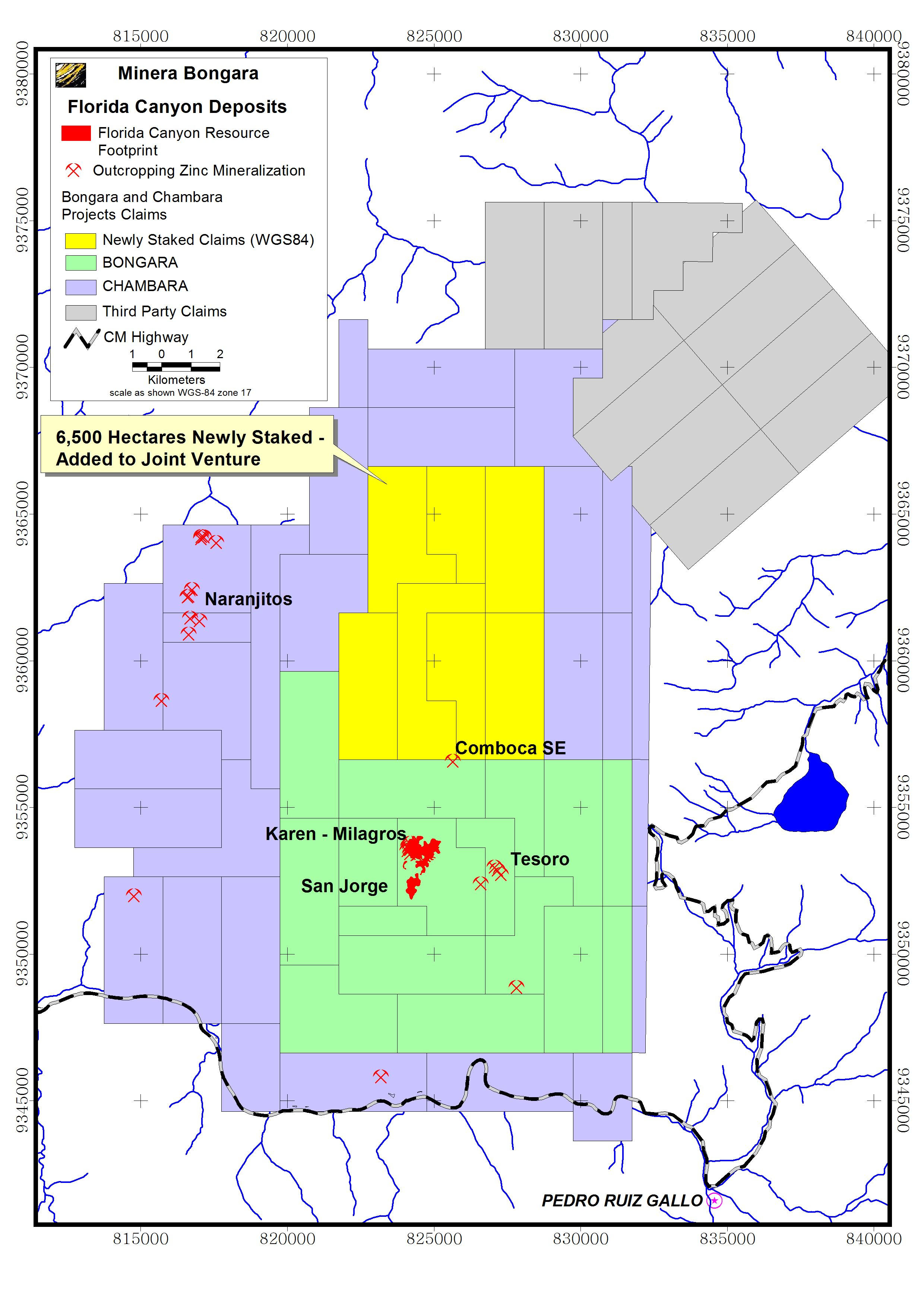

- Bongará is comprised of 16 contiguous mining concessions, covering approximately 12,600 hectares. In the image below, you can see the “newly” (at the time of the technical report) staked ground, which is on trend with the rest of the deposit and may provide some upside to the resource size with further exploration.

Source: Solitario

- The mineralization is polymetallic and of Mississippi Valley Type (MVT). To note, it’s expected to be an underground mine.

- Bongará is a Joint Venture project between Solitario and Milpo.

- Currently, Solitario owns 39% of the project, but Milpo can earn up to a 70% interest in the project by funding all project expenditures and, based on a positive feasibility study, commit to putting the project into production. Also, Milpo will finance Solitario’s 30% portion of the construction costs via a loan, which will be paid back with 50% of its net cash flow distributions, once in production.

- More than 80% of Milpo’s publically traded shares are owned by Votorantim, Solitario’s former JV partner. In 2014, Milpo announced its intent to acquire Votorantim’s share of the Bongará Project. Milpo is the 2nd largest zinc producer in Peru, operating 3 other underground zinc mines and, from my perspective, is the perfect JV partner for this project.

PUSH: A Preliminary Economic Assessment (PEA) is expected to be completed by the end of July 2017. The PEA should bring some much needed attention to the Solitario story, especially given its upside to a rising zinc price. What really strikes me is that Milpo did not have to jointly fund this PEA, which makes me think they’re confident that the PEA is going to show a lot of value in this deposit and, from a promotional side, is well worth the money.

Resource Estimate

Measured and Indicated Resource Total: tonnes – 2.78 million, Zn% – 12.77, Pb% – 1.78, Ag g/t – 18.2, ZnEq% – 15.1 – Contained metal: Zn Mlbs – 782.5 Inferred Resource: tonnes – 9.07, Zn% – 10.87, Pb% – 1.21, Ag g/t – 12.2, ZnEq% – 12.44 – Contained metal: Zn Mlbs – 2,173 Metal price assumptions in USD: Zn – $0.95/lbs, Pb –$0.95/lbs, Ag – $20/oz

NOTE: These are great zinc resource numbers, with both size (Total M&I + Inferred Zn contained metal = 2,955.5 Mlbs) and grade. The metal price assumptions are good, especially with upside in the zinc price. Also, as described in the Technical Report, mineralization is open and provides exploration upside to an already large high grade deposit.

What is Solitario’s portion of the Bongará mine worth? Until the PEA is complete, which will be soon, we really don’t know. Not all in-situ metal is created equal and, therefore, makes it tough to realistically compare Bongará to other zinc projects in the world.

NOTE: Solitario’s 30% of Bongará is currently equivalent to: (925.3 Mlbs + 2,487.6 Mlbs) x 30% = 1,023.87 Mlbs of Zinc Equivalent.

However, I think the value proposition is fairly straightforward. Solitario has a tight share structure with roughly half of its MCAP in cash, therefore, not even considering Solitario’s other interests, you can see that the value per lbs, in USD, is roughly $0.011/lbs. That’s very cheap, in my mind, and I’m sure that the upcoming PEA will confirm this.

- The metallurgy of the deposit appears to be in good order as the predicted concentrate grades are as follows: Sulfide – concentrate Zn% – 55.2, Pb% – 52.6, Ag g/t – 7.3 Mixed – concentrate Zn% – 52.0, Pb% – 52.6, Ag g/t – 7.3 Oxide – concentrate Zn% – 47.5

- Comments regarding the metallurgy of the mineralization from the Technical Report,

“the high in-situ grades of the zinc mineralization and low impurities in sulfide at Bongará should generate a premium concentrate and a highly saleable product in a market where strong future demand is forecasted. The challenge to Project development lies in its remote location, which raises capital costs for construction and operating costs for concentrate delivery, among other things.” ~ 43-101 Technical Report – pg.137

- In my discussion with CEO, Chris Herald, he mentioned that one of the highlights of the Bongará Project is how clean the metallurgy is. The future mine should produce a top notch concentrate, one that will have smelters lining up to purchase it. This is really important when it comes to zinc deposits, because there’s a good portion of deposits out there that have mercury, iron or manganese issues with their concentrate, and require much more refinement to produce something saleable. In my opinion, metallurgy is arguably the most important attribute of any mineral deposit, not just zinc. So the fact that the Bongará metallurgy checks out is a big plus.

Peru as a Jurisdiction

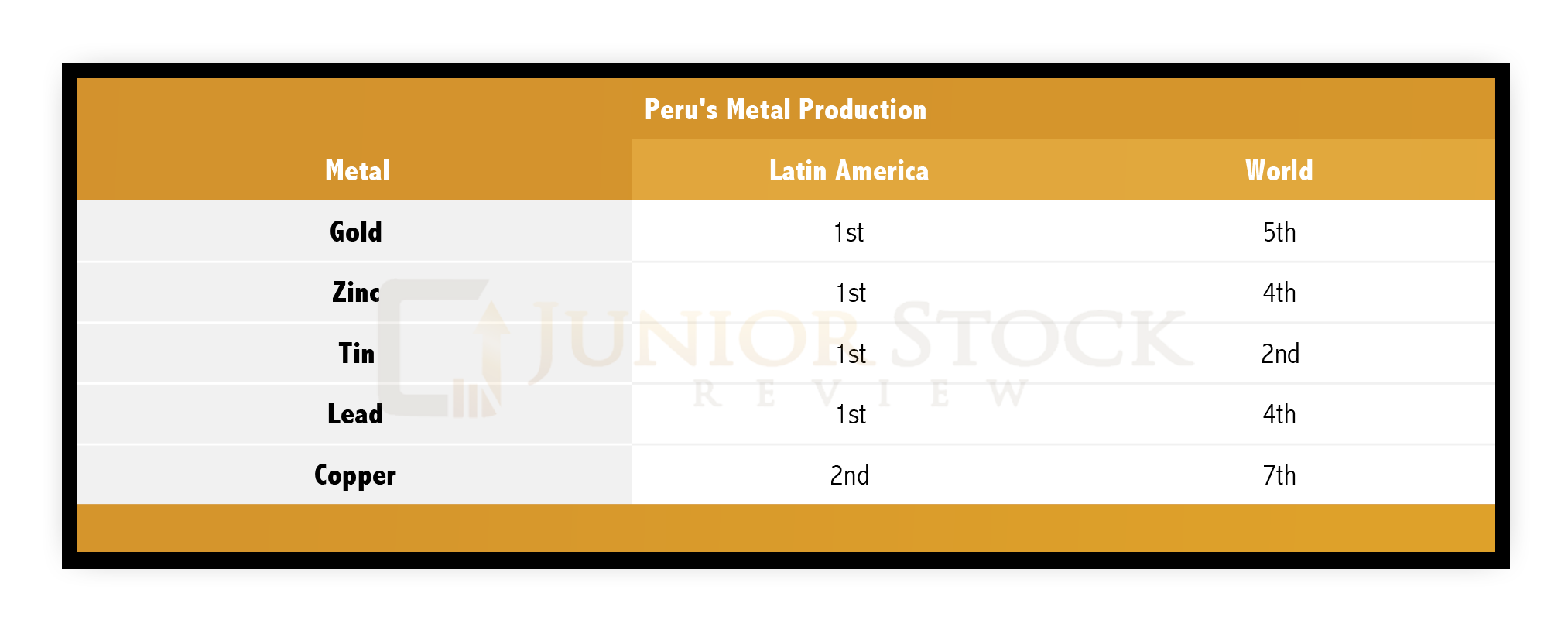

In its latest rankings, the Fraser Institute lists Peru as the #1 jurisdiction for mining investment attractiveness in Latin America, with a score of 73.47 and 28th in the world. Mining is a major source of employment for the Peruvian people; as you will see in the table below, Peru ranks not only tops for metal production in Latin America, but also close to the top in most categories throughout the world.

~ Source: Mining Peru

“[T]he mining industry believes that Peru’s favourable geology has been under-exploited…to date only about 12 per cent of Peru’s mineral resources have been worked…In all, Peru holds about 16 per cent of the word’s known mineral reserves, including 15 per cent copper and 7 per cent zinc reserves.”~ Mining Peru

Peruvian Leadership

The Prime Minister of Peru is determined in a two round election system. A two round system works in the following manner; a single vote is cast for their chosen candidate. If no candidate receives the majority of the votes, usually 40 to 45% of the vote and a margin of 5 to 15%, all but the two candidates with the largest percentages are eliminated and then placed into a second election.

2016 was an election year in Peru. The Congressional election saw the Party, Popular Force, win in a landslide, taking 36.34% of the vote (~Peruvian Election Results). However, the Prime Minister election, which took two rounds to decide, went to the Party, Peruvians for Change, which is led by candidate, Pedro Pablo Kuczynski.

Kuczynski has held positions in the United States with the World Bank and the International Monetary Fund. He later became Peru’s designated general manger of its Central Reserve Bank. From the standpoint of an investor, I believe that Kuczynski’s western influenced work experience should prove to be an asset.

Will he be good for the Peruvian people? Hard to say, as developing a country’s economy is a costly business (debt) these days. But, if done properly, it could be the dawn of a new age for the Peruvian people, and may bring what is currently a third of the population, out of poverty.

My guess is that Kuczynski will be good for mining and, as a western investor, I’m comfortable with the risk that Peru’s leadership presents.

43-101 Technical Report – Peru as a Jurisdiction

SRK Consulting, the company that prepared the 43-101 Technical Report, has a great section discussing property and title in Peru:

“Mining in Peru is governed by the General Mining Law, which specifies that all mineral assets belong to the federal government. Mining concessions granted to individuals or other entities authorize the title holder to perform all minerals related activates from exploration to exploitation and, once titled, are irrevocable for so long as the fees are paid to the federal government on time.” ~43-101 Technical Report – pg.7

SRK Consulting also comments on the Peruvian workforce in relation to Bongará Project,

“No trained mining personnel reside near the Project. Untrained labor is readily available from local communities where few employment opportunities exist. Peru is a mature mining country with a mobile workforce. Abundant trained labor is present in all categories of mining throughout Peru. “ ~ 43-101 Technical Report – pg.8

The first thing that comes to mind when I read this is, “if you build it, they will come.”As cheesy as that may sound, Peru is a country that depends on mining for employment and, therefore, I do believe that when the time comes, a workforce will be available.

Source: U.S. Geological Survey

Peru is a country on the rise, as it has grown its economy at a rate of 6.4% annually, on average, for the last 10 years, which is 2nd among Latin American countries (~ Peru). The service industry represents the largest chunk of the country’s GDP, with agriculture following a close second. Mining follows these top two industries and looks set for growth in the coming years, with further development of its prospective mining properties.

As Peru looks to further its economic growth, in my mind, mining will have to constitute a major part of their future. Therefore, while not without risk, Peru does present great value from a jurisdictional standpoint, today and into the future.

NOTE: In relation to Solitario, remember that its majority owner, Milpo, the 2nd largest zinc mine operator in Peru, is handling development of the property and, thus, in my mind, reduces the risk associated with a foreign entity developing or operating the property.

Zazu Acquistion – Lik Property

- Solitario, upon approval of the purchase, will acquire all of the issued and outstanding shares of Zazu Metals Corporation. It is an all shares deal wherein holders of Zazu shares will receive, on closing, 0.3572 of a common share of Solitario, which represents a 41% premium over the VWAP20 of Zazu. Zazu shareholders are expected to represent approximately 34% of the issued and outstanding shares of the combined company. See the news release for the exact details of the transaction.

- Zazu acquired a 50% interest in the Lik property for $20 million in June 2007, from GCO Minerals. The remaining 50% of the project was and still is held by Teck Resources. The terms of the GCO agreement carried over to Zazu, which has the option to acquire an additional 30% of the property by qualifying expenditures of $20 million prior to 2018. See Technical Report or SEDAR for further information.

Further, in my email correspondence with IR, I asked, ‘how much money must be spent by Solitario to attain the additional 30% in the Lik property?’

“Approximately $20 million…If we don’t spend the $20 million, then Solitario will own 50% of the Lik Project and will continue to be the operator.”

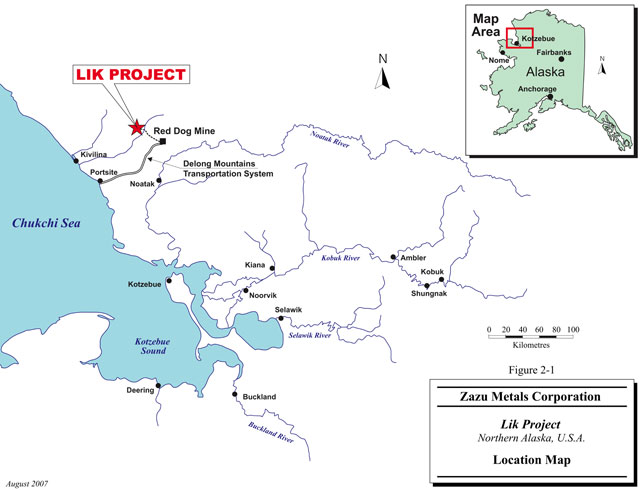

- The Lik property is located in Northwest Alaska, 22 km from Teck Resources’ Red Dog Open Pit Mine.

Source: Zazu Metals

- The Fraser Institute’s ranking for Mining Investment Attractiveness gives Alaska a score of 80.27, placing it 5th amongst the American States, and 14th in the world. Even with this great ranking, at this current time, Alaska may still be associated with the highly publicized issues between Northern Dynasty and the EPA over their Pebble Project. Isolated incidents such as this can be present in the best of jurisdictions, as the score gives a broader view on the jurisdiction on a whole. Proximity doesn’t mean that the Lik property is guaranteed to be approved for the construction of a mine, but Teck’s Red Dog mine is only 22 km away and has been operating for a long time. I’m confident that permitting won’t be an issue.

- The Lik deposit is divided by faulting into two parts, Lik South and Lik North. The PEA that was completed in 2014 was on the Lik South Deposit, which they believe can be mined in an open pit. The Lik North Deposit is much deeper than the South and will most likely require underground mining techniques for its removal.

- Original drilling (137 holes) of the project occurred in the 1970s, 80s, and early 1990’s with some historical mineral resource estimates completed by GCO and Noranda. Zazu completed an additional 92 holes from 2007 to 2011.

- Total Mineral Resource Estimate (North and South Deposits) taken from PEA Report: Indicated:Mt – 18.11, Zn% – 8.1, Pb% – 2.72, Ag g/t – 50.2 Inferred: Mt – 5.34, Zn% – 8.66, Pb% – 2.69, Ag g/t – 38.0 (See the PEA for further details)

- The PEA was completed for the Lik South Deposit ONLY

- After Tax NPV @8% – USD $25 million, IRR – 9.7%, 5.8 year Payback, CAPEX Cost – $351.7 million Metals Price Assumptions in USD – Zn – $0.9242/lbs, Pb – $1.013 lbs, Ag – $19.43/oz – At first glance, this may seem low, but remember this is a high-grade zinc project and, therefore, should present a high sensitivity to the zinc price. The PEA lists revenue associated with each metal as approximately 70% zinc, 29% lead and 1% silver on pg.1-16.

- In Zazu’s corporate presentation on page 16, a price sensitivity table reveals the upside potential of the project. Using today’s zinc price of roughly $1.12 per pound, and the project After Tax NPV @8% jumps to USD $195 million, IRR – 20.0%, Payback 3.4 years.

- The Lik Property PEA envisions a 5,500 tpd mill, with a CAPEX cost of $352 million, including a 20% contingency. Again, remember that this only concerns the South deposit.

9.97% Equity Interest in Vendetta Mining

– On May 5th, 2016 Solitario announced a strategic 9.97% equity investment in Vendetta Mining. Solitario purchased 8,000,000 units of Vendetta for a total consideration of CDN $362,000, with each common share priced at CDN $0.05, and one full warrant with a two-year term, and exercisable at CDN $0.10. Please see SEDAR for more detailed information regarding the financing.

– This investment shows great foresight by Solitario’s management into the zinc market and the potential of Vendetta Mining, which has seen great gains in its share price since their purchase.

– While I like this investment, it’s a much smaller piece of my speculative thesis regarding Solitario. I have compiled some notes on Vendetta Mining because I really like their story and its potential, but I will publish those in a separate article. If you aren’t already a subscriber and don’t want to miss that article, become a Junior Stock Reivew VIP and have the article sent to your inbox for FREE.

Solitario’s Remaining Royalties

While Solitario does have additional royalties, I haven’t considered their value at their current stage of development. Nonetheless, here’s a list of Solitario’s 3 other royalties:

- Pedra Branca Platinum/Palladium Project – Solitario retains a 1% royalty

- Montana Royalties – 1.5% NSR on 11 properties

- Yanacocha NSR Royalty Project

Concluding Remarks

There’s always downside risk in any speculation that you make. In the case of Solitario, I think the current downside risk comes from the potential for the zinc price to fall. That said, a lower zinc price wouldn’t make their projects uneconomic, it would likely result in losses for zinc companies overall. Secondly, due to a lack of promotion, the stock is being thinly traded at just below 10,000 shares on the TSX per day and 58,000 on NYSE-MKT. However, I view this in a positive light; I relish the opportunity to buy shares of a company before their story catches on in the mainstream. I expect post-transaction, that Solitario will want to get their new story out to the investment community.

For me, the release of the Bongará PEA in the next month or so and the confirmation of the Zazu purchase will be turning points for attention on Solitario, and will allow investors to put a proper valuation on this company. Now, with a MCAP of around $39 million, it’s undervalued, especially in context to the supply and demand fundamentals of the zinc market.

To summarize my reasons for buying shares of Solitario:

- An experienced management team which seeks and capitalizes on value in the market – without major shareholder dilution.

- PUSH from an upcoming Bongará PEA, which I believe will shine a very bright light on this large and high-grade zinc deposit.

- Bongará JV partner, Milpo – an experienced zinc mining company, which is set to cover all expenses and technical work on the project right up to the commitment for mine construction. The 30% interest in Bongará comes at no upfront capex cost to Solitario, just the repayment of Milpo-funded construction costs paid from operating cash flow. Consequently Solitario will receive cash flow starting day-one of production without dilution.

- Upon closing the deal – Lik Property JV partner, Teck – large senior multi-metal miner, which I would guess will be motivated to see development of this Alaskan deposit, as their massive Red Dog Mine will see reduced production numbers in the years ahead, right in the face of a supply shortage in the zinc market.

- Leverage to higher zinc prices – Both the Bongará and Lik Projects are highly sensitive to a rising zinc price.

- A good sized position in a highly prospective zinc exploration company – Vendetta Mining, which is currently worth: $0.34/share x 8,000,000 shares = $2,720,000. There are 5,000,000 Cdn $0.10 warrants, too!

- CASH – Solitario is sitting on roughly USD $17 million – almost half of their market cap – to my knowledge, ONLY Arizona Mining, amongst zinc companies, has a larger cash position.

Do your due diligence on Solitario and see if they are a company that fits your speculative criteria. For me, they present a great risk to reward speculation, especially going forward, as I’m confident that even if we don’t see higher zinc prices, there is still great value in this company.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: This is not an investment recommendation, it is an investment idea. I am not an investment professional, nor do I know you and your specific investment criteria. Please do your own due diligence. I have NOT been compensated to write this article and do NOT have a business relationship with Solitario Exploration & Royalty. However, I do own shares in Solitario Exploration & Royalty. Please check SEDAR for the most accurate data regarding Solitario Exploration & Royalty information and analytics.